Assessing Liquidity Risk in DeFi

To date, decentralized finance (DeFi) has successfully scaled financial markets built on highly liquid collateral. Near instant settlement has been a key feature of effective lending markets, automated market makers, collateralized stablecoins, and vanilla vault strategies. As a result, much of today’s DeFi infrastructure implicitly assumes that assets can be converted into cash quickly and predictably.

As DeFi continues to mature, it has expanded into fixed-rate lending, real-world assets (RWAs), cross-chain settlement, and complex vault strategies. The implicit assumption that assets can be quickly and predictably converted into cash (that they are “liquable”) begins to break down. This more mature DeFi presents users with liquidity risk, the possibility that capital cannot be converted to cash or collateral without material loss or delay.

Liquidity risk has become a core concern in DeFi, shaping how assets are composed, priced, and ultimately deployed across lending markets, vaults, and tokenized RWAs. For market participants across the stack, the ability to assess, manage, and price liquidity risk is critical to scaling structured products onchain.

This report provides a comprehensive view of liquidity risk in DeFi. It examines what liquidity risk is, where it arises, how it affects composability, how it’s priced, and how different asset durations should be categorized. Finally, it explores emerging approaches that allow this risk to be separated, traded, and managed more explicitly within the DeFi ecosystem.

What Liquidity Risk Means Onchain

A useful way to understand liquidity risk in DeFi is through the concept of time-to-cash: the time between when a holder requests liquidity and when funds are actually received. This interval may include redemption notice periods, settlement processes, withdrawal queues, or other operational delays embedded in the design of a protocol or financial instrument.

Assets with longer time-to-cash carry higher risk. The longer the lock-up, the higher the yields investors require to compensate them for the illiquidity. This is known as an illiquidity premium.

Secondary markets can help provide liquidity, but they often introduce their own risks such as fragmented liquidity, slippage, exit fees, or deep discounts. Many consider this to be a “cost layer, not a feature.”

For asset managers, this creates portfolio constraints. As we discuss below, liabilities in DeFi are often effectively instant (in the form of withdrawable deposits or on-demand redemptions), creating demand for assets with matching liquidity. For onchain asset managers, managing liquidity risk on both sides of the balance sheet has become a critical core competency.

“Even long term investors will hesitate to allocate to an asset if they have concerns that, on the day liquidity is needed, exits will be slow, capped, or heavily discounted.“ - Keith Selover, Steakhouse Financial

Key Sources of Liquidity Risk in DeFi

RWA Redemption Timelines: RWAs inherit the redemption cadence of underlying TradFi instruments. These can be near-instant (but not atomic) in some cases such as BlackRock’s BUIDL fund which offers T+0/T+1 liquidity on T-bills via a USDC liquidity pool. On the other hand, traditional private-credit and bond funds typically impose longer redemption windows, and tokenized versions often retain this structure. For example, Apollo’s ACRED private credit token remains gated by quarterly redemptions with periodic redemption caps. In practice, these slow windows mean an investor can’t easily liquidate on demand.

Staking Withdrawal Queues (LSTs/LRTs): Liquid staking tokens (LSTs, LRTs) promise liquidity for staked crypto, but the underlying network mechanics for staking still produce exit delays. After Shanghai, validators can only exit at 256 per epoch, causing backlogs. In 2025, the queue reached 2.65M ETH, with estimated withdrawal times peaking at 46 days. Lido and similar LSTs could not bypass this, forcing vaults and protocols holding stETH to endure a multi-month liquidity freeze.

Vault Withdrawals: Many ERC-4626 vaults allocate most capital into strategies, leaving little idle cash for redemptions. While high utilization can be a sign of efficiency, a vault where only 10% of cash is immediately available, for example, would stall under heavy withdrawal pressure. If many users redeem at once, the vault must unwind positions (at a loss or delay) or ration liquidity. Most vaults are async and have withdrawal delays that range from minutes to days while some vault designs even introduce short lock-up periods to manage this risk. In general, high utilization creates an asset-liability mismatch and delayed liquidity.

Cross-chain Withdrawal Delays: Assets moved across chains often incur delay by design. For example, participating in optimistic rollup L2s such as Arbitrum and Optimism enforce a 7-day “challenge period” on withdrawals. Similarly, some cross-chain bridges or IBC transfers have lock-ups ranging from hours to days. Therefore, DeFi protocols spanning multiple chains must account for days of illiquidity in cross-chain settlements.

Offchain Liquidity Deals: Some protocols augment onchain TVL with offchain commitments such as enterprise staking services and institutional deposit facilities. These can boost TVL but may leave a gap if counterparties fail or delay offchain withdrawals. While hard to quantify, any reliance on offchain funds introduces redemption uncertainty if counterparties renege.

Fixed-Rate Lending: Fixed-rate lending products intrinsically lock capital for set terms from weeks to months. Users deposit funds for a fixed term and fixed yield and early exit is typically not allowed or carries penalties. This creates liquidity risk. Lenders must wait full term, and if they need funds earlier they lose returns. Thus fixed-rate lenders demand a higher yield compared to variable-rate markets where capital can withdraw anytime. This makes fixed-rate loans hard to scale, as liability-matching and high required yields deter short-term depositors.

How Liquidity Risk Affects Composability

DeFi’s composability depends on liquid collateral and most DeFi primitives assume instant liquidity of underlying assets. Lending protocols, vaults, and stablecoins are built around collateral that can be liquidated quickly onchain. Illiquid assets break these assumptions.

For example, Aave’s Horizon RWA market for permissioned institutional assets initially only accepts short-term collateral, namely short-dated treasury and CLO funds. Circle’s USYC short-duration T-bill fund and Superstate’s USTB/USCC short U.S. debt and yield funds were chosen so that maturity and redemption align with Aave’s needs.

This reflects the broader challenge: most DeFi systems struggle to integrate long-duration RWAs because automated liquidation is impractical. As a result, few DeFi markets accept multi-month bonds or quarterly-redemption funds as collateral. Similarly, fixed-rate lending markets have seen limited adoption since lenders expect substantially higher rates, which can suppress demand.

In practice, DeFi’s has a short-term bias because of liquidity risk.

The result is that long-duration assets require bespoke hedges, liquidity overlays, and liquidation agreements. For instance, to loop long-term RWA collateral one must construct extra liquidity buffers or use derivatives. Without such mechanisms, heavy withdrawals or liquidation triggers would break protocols.

The examples go on. Similar principles apply to many asset classes that would be unable to tap into the utility of DeFi. DeFi’s maturity thus depends on developing tools for liquidity risk: markets, insurance, or pooled liquidity that can absorb illiquidity without crashing. This remains a key unsolved challenge for scaling DeFi to onboard traditional finance assets, which often carry significant lock-ups.

If DeFi wants to support RWAs, vaults, and structured credit at scale, it needs more than tokenization. It needs a way to disambiguate different risk and allow pricing on specific ones like liqidity risk. then it can underwrite that risk directly. That is the infrastructure layer that unlocks the next phase of growth and make DeFi more scalable." — Phil Fogel, Cork

Pricing Liquidity Risk

As we’ve seen, assets with higher liquidity risk generally demand higher yields. For example, we can say that staking yields such as 2-3% on ETH essentially compensate for the illiquidity of the underlying asset. The remaining question then is how do we determine that liquidity premium?

A rigorous pricing of DeFi liquidity risk would involve scenario modeling, estimating expected shortfall from forced sales, and then computing what extra yield would satisfy rational lenders.

In practice, DeFi protocols have opted for other frameworks that carry less complexity and computational overhead. They can implement layered liquidity that segments risk by instant, short-term, and long-term windows to reduce pricing inefficiencies. In broad terms, this lets us think about risk in the following way:

Short Duration (1–7 days): Essentially cash-like. Examples include true stablecoins (redeemable on demand), tokenized short-term Treasury funds, and assets with at most one-week exit. These instruments guarantee swift redemption and sometimes come with deep secondary markets, so their liquidity risk is very low.

Intermediate Duration (~1–3 months): Assets that require moderate notice. Examples are open-ended real-world funds with monthly windows, fixed-term lending positions (30–90 day notes), or vault strategies with 2–4 week lock-ups. These may have some secondary trading, but it’s limited. Under stress, liquidating these assets may incur noticeable slippage or short-term loss, so a modest liquidity premium applies.

Long Duration (Multiple Quarters–Years): Assets with long lock-ups and sparse liquidity. This includes venture funds, tokenized multi-year bonds, and certain credit funds. Traditional private-credit funds often only offer quarterly redemptions. For example, a private-credit token might only allow redemptions each quarter, then require 30+ days to settle. Secondary markets for these are very shallow. Consequently, they command the highest yields to compensate for illiquidity and term risk.

Market participants already assess liquidity risk with a framework based on this view. Steakhouse’s use of Morpho implements a three-layer liquidity stack that consists of atomic redemptions, discount-window liquidity, and monthly redemptions. This mitigates price slippage and minimizes the possibilities of accruing bad debt to lenders.

By framing assets in these categories, a DeFi risk analyst can apply graduated pricing: cash-like assets may be priced near the risk-free curve, whereas long-duration credit-like assets get steep liquidity spreads.

Framework for Analyzing Liquidity Risk

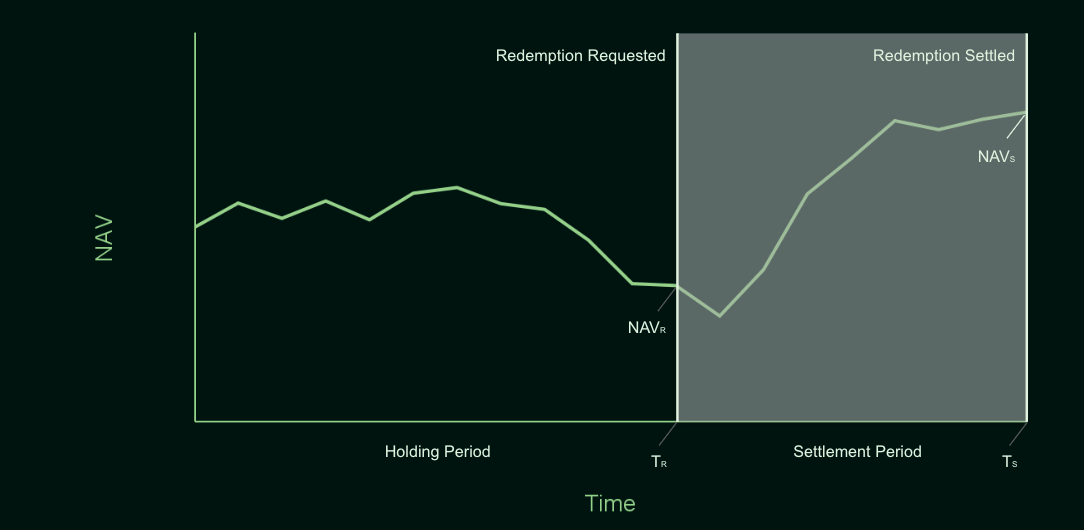

To help frame our analysis, below is a simplified graphic showing an RWA’s NAV over time.

RWA NAV over time

A user holds the RWA over the Holding Period, submits a redemption request at time TR, and following a Settlement Period, receives settled funds at time Ts.

Any comprehensive framework for evaluating Liquidity Risk should consider:

Settlement Period Analysis: After a redemption request is made, how long does it take for the holder to receive funds? Is the length of the settlement period known at the time of redemption (ex: reliability two business days) or is it variable (ex: one to three business days, depending on the operational needs of the issuer)?

Pricing Changes During the Settlement Period: For some RWAs, redeeming holders receive NAVR (the NAV when the redemption request is submitted), providing certainty of proceeds upon settlement at Ts. For other RWAs, holders receive NAVs (the NAV when the redemption actually settles), meaning the final redemption value is unknown at the time of submission.

Receiving the Redemption NAV (NAVR): Settling at NAVR shifts interim price risk from the redeeming holder to the issuer, insulating the holder from the risk of price declines. Conversely, the holder forgoes any appreciation or accrued income during the settlement period, tying up capital without an opportunity for return. As detailed below, any holder should consider the opportunity cost of capital from tying up funds during this period.

Receiving the Settlement NAV (NAVS): Settling at NAVS leaves the redeeming holder economically exposed until settlement. For these RWAs, it is helpful to know if a redemption request can be withdrawn once it is made. From the issuer’s standpoint, NAVS reduces mismatch risk by aligning redemption proceeds with the realized value of underlying assets at settlement, strengthening liquidity management and improving the likelihood that redemption obligations can be met without strain.

Liquidity Coverage Provisions: Liquidity risk can be mitigated through explicit coverage mechanisms. Some systems maintain liquidity pools that allow investors to exit positions immediately, even when the underlying assets require longer to settle. In the example above, the RWA issuer would maintain a liquidity sleeve allowing some portion of RWA holders to redeem on demand at time TR.

Secondary Market Depth: Even when primary redemption is slow, active secondary markets can provide additional exit routes. Analysts should therefore examine trading activity across decentralized exchanges, liquidity pools, and over-the-counter markets. In the example above, the RWA holder could look to sell their position at TR if secondary pricing was sufficiently close to NAVR, bypassing the need to redeem at all.

Opportunity Cost of Capital: Quantify what alternative return was forgone by locking funds. For example, if 6% was available on stablecoin lending, an illiquid 8% loan actually carries only a 2% net premium. This helps calibrate how much extra yield is truly compensatory.

Stress Testing: Finally, liquidity risk analysis should include stress testing under adverse scenarios. For example, analysts may simulate what happens if a large share of investors attempts to redeem simultaneously. By examining available liquidity buffers, market depth, and redemption limits, it is possible to estimate how long it would take for investors to exit and what price impact might occur.

A robust framework treats liquidity as a first-class risk factor, akin to credit or market risk. Effective analysis uses both quantitative (order book depth, redemption notice periods) and qualitative (governance or protocol guarantees) inputs. The goal is to ensure that any yield spread assigned to an asset properly reflects the full cost of potential illiquidity under all plausible scenarios.

Structuring and Pricing Risk Tokenization

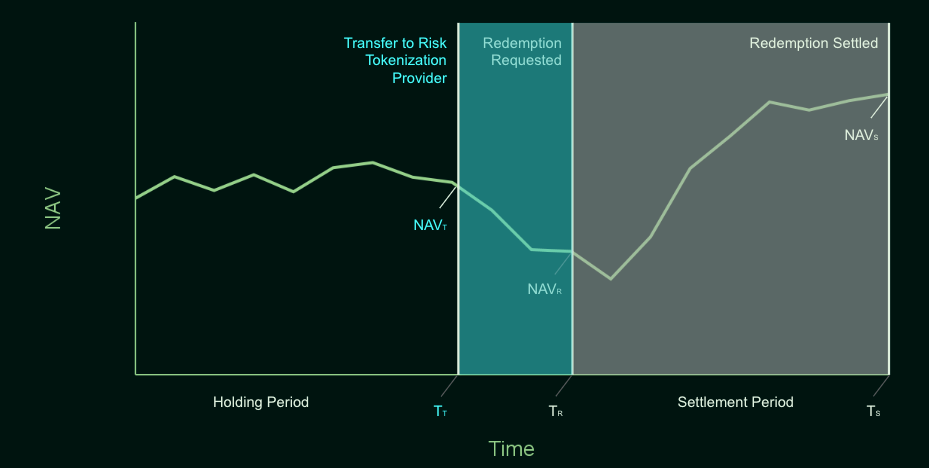

Furthermore, we can take this framework a step further and use it as the basis for the tokenization of risk through a Risk Tokenization Provider. The tokenization of risk would in turn enable risk to be explicitly priced, traded, and used as a primitive within markets. More importantly, tokenized risk can act as a liquidity buffer.

Below we expand on our earlier chart, to provide an example of how a Risk Tokenization Provider might participate in a redemption.

Risk Tokenization Provider in redemption process

Instead of redeeming the RWA with an issuer directly, a user would elect to transfer that RWA to the Risk Tokenization Provider, accessing instant liquidity and bypassing the redemption process altogether. At time TT the Risk Tokenization Provider would take possession of the RWA, becoming responsible for the ultimate redemption.

The Risk Tokenization Provider inherits all of the considerations discussed above in “Framework for Analyzing Liquidity Risk”. The Provider absorbs NAV volatility, redemption uncertainty, and potential duration extension in exchange for a fee.

For RWA holders, the Provider transforms an uncertain time-to-cash profile into instant liquidity for the exiting holder. The design space for compensating the Provider is flexible, but below, we’ve included two primary constructs:

Commitment Fees:

A Risk Tokenization Provider makes a commitment to take ownership of an RWA on demand, at agreed upon transfer pricing terms. To fulfil that commitment, the Provider must reserve capital that can be deployed immediately on demand, up to its full commitment amount. In exchange for this capital commitment, the Provider would assess a “commitment fee”, charging potential users an upfront cost for the opportunity to access the Provider’s capital later on.

This structure has precedents in the world of traditional finance. Committed Liquidity Facilities (such as those offered by the Reserve Bank of Australia), Revolving Credit Facilities (such as those utilized in asset-backed lending), or vanilla letters of credit all feature some kind of upfront fee, compensating liquidity providers for their commitment.

Discounts to NAV on Transfer:

In addition to an upfront fee, a Provider can be compensated through a discount embedded in the transfer price at time TT. Instead of acquiring the RWA at NAVT, the Provider would acquire the RWA at some haircut to NAVT. This increases the probability that the Provider will earn a gain-on-sale when it redeems the asset with the issuer at Ts.

The magnitude of the discount can be informed by historical NAV drawdowns for the underlying RWA, the anticipated holding period for the Provider, the Provider’s assessment of macro-economic conditions, and the amount of time the asset will have to be held before it can be redeemed.

This structure resembles several instruments in traditional finance, including tender option bonds (in municipal markets), or floating-strike put options (where the strike adjusts based on prevailing asset values).

Turning to ACRED

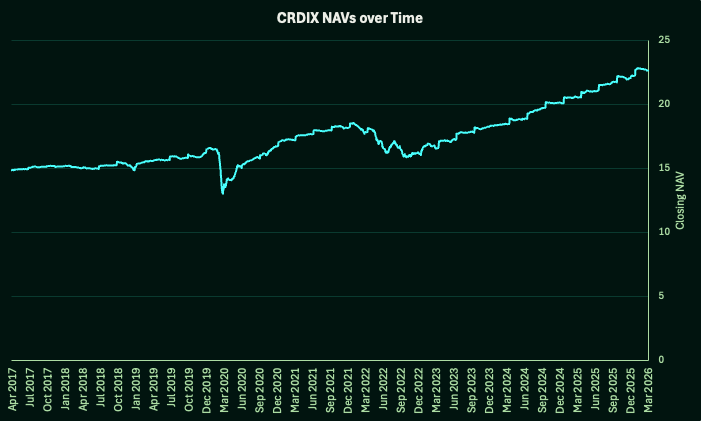

ACRED is a tokenized representation of Apollo’s Diversified Credit Fund (CRDIX), a private credit strategy that primarily invests in directly originated corporate credit opportunities. The underlying CRDIX fund holds a diversified portfolio of senior secured loans and other private credit instruments designed to generate stable income while maintaining portfolio diversification.

Tokenization allows exposure to the CRDIX strategy to be represented onchain while preserving the core investment and redemption mechanics of the underlying fund structure. ACRED inherits many of the liquidity characteristics of CRDIX as a result, including periodic redemption windows and settlement timelines that reflect the liquidity profile of the underlying assets.

ACRED NAV over time

The chart above illustrates the historical evolution of CRDIX’s net asset value, including periods prior to Apollo assuming management of the strategy from Bain Capital Credit. While the fund has generally exhibited a relatively stable return profile, periods of broader market stress (such as those observed in 2020 and 2022) did result in observable NAV volatility. These periods are relevant when considering the pricing of liquidity risk.

Redemptions and Queue Risk

ACRED inherits the redemption mechanics of the underlying Apollo Diversified Credit Fund (CRDIX), which is structured as a 1940 Act interval fund. Shares of the fund are not listed on an exchange, and liquidity is provided through periodic repurchase offers conducted by the fund.

Under this structure, the fund conducts quarterly repurchase offers during which shareholders may submit requests to redeem shares. Each quarter, the fund offers to repurchase no less than 5% of its outstanding shares at net asset value (NAV).

If redemption requests exceed the size of the repurchase offer, requests are satisfied on a pro rata basis. In practice, this means investors may receive only partial liquidity in a given quarter, with the remaining portion of their request carried forward to subsequent redemption cycles.

Investors seeking to fully exit their position may need to participate in multiple redemption windows before their entire position is redeemed. This introduces queue risk: the possibility that an investor’s effective time-to-cash becomes extended if aggregate redemption demand exceeds the quarterly repurchase capacity of the fund.

Redemption Pricing and Withdrawal Rights

Repurchases occur through discrete quarterly cycles with a defined request deadline, pricing date, and payment date.

For example, the most recent quarterly Redemption Request Deadline Date was February 3, 2026. Investors were able to submit redemption requests beginning December 24, 2025 and continuing until that deadline. A holder may withdraw their redemption request at any time prior to the deadline.

The redemption price is not fixed when the request is submitted. Instead, shares are repurchased at the NAV determined on the Repurchase Pricing Date, which occurs no later than 14 days after the Redemption Request Deadline.

As a result, investors submitting redemption requests remain economically exposed to NAV movements between the time the request is submitted and the pricing date, while retaining the ability to cancel the request prior to the deadline if conditions change.

Implications for Liquidity Risk Management

ACRED’s redemption structure makes it a natural candidate for liquidity underwriting through risk tokenization.

For ACRED, the effective time-to-cash is uncertain. While the fund conducts quarterly repurchase offers, the 5% cap on redemptions means that investors may need to participate in multiple redemption cycles if demand exceeds available capacity.

More importantly, the final redemption price is determined at settlement, leaving redeemers exposed to NAV movements while their request remains outstanding.

A Risk Tokenization Provider could absorb these risks by acquiring ACRED tokens from exiting investors and holding them through the redemption process. In doing so, the provider assumes the uncertainty around redemption timing, queue dynamics, and interim NAV volatility.

To underwrite this exposure, the provider would need to determine an appropriate discount to NAV and commitment fee reflecting both the fund’s redemption mechanics and the historical volatility of CRDIX. As discussed in the stress testing section above, this analysis would likely consider how the strategy’s NAV behaved during periods of market stress such as 2020 and 2022 and what holding the asset through those environments would have implied for their returns.

Current Developments: Risk Tokenization as a Liquidity Layer

Markets like ACRED would benefit from risk tokenization as a solution that escapes a skeuomorphic interpretation of risk that seeks to simply translate or imitate traditional models onchain. Here, we can take an onchain-native approach and tokenize risk altogether, price it, and separate it from the reference asset. This lets us build liquidity buffers that effectively quantify illiquidity. In essence, it’s a form of alchemy where long-duration assets can take on short-duration properties and act like highly liquid assets.

Cork is pioneering a tokenized risk layer that enables pricing and trading of illiquidity exposure itself. By separating the liquidity risk from the underlying asset, Cork allows vaults and investors to hedge or underwrite risk dynamically. A tokenized risk primitive can:

Represent illiquidity premium as a tradeable instrument on both sides of the trade

Enable on-chain pricing of redemption timelines

Provide structured protection for vault redemptions

For managers like Steakhouse, this means vaults can hold long-duration RWAs while transferring the liquidity risk to a separate pool of underwriters. This creates a path toward scalable, resilient, and composable yield vaults in DeFi.

Learn more about Steakhouse and Cork:

Website: Steakhouse | Cork

X: Steakhouse | Cork

Newsletter: Steakhouse | Cork

Contact us: Steakhouse | Cork